Retirement Planning From a Behavioral Health Perspective

|

|

Gerontology

A Training Resource

By Jim Messina, Ph.D., CCMHC, NCC, DCMHS-T

|

|

|

“What it takes to be a Retirement Transition Counselor”

Webinar - Florida Mental Health Counselors Association

February 12, 2021

|

Implications of Retirement on the Mental Health of Seniors

Facts about the future role of Retirement in the Life of the USA and the World

The world is undergoing a massive demographic shift. More than 70 million

baby boomers will retire in the next 20 years in the United States alone. By

2035, Americans of retirement age will exceed the number of people under the age of

18 for the first time in US history. Globally, the number of people age 60 and

over is projected to double to more than 2 billion by 2050 (Haanen, 2019)

|

A Historical Perspective on Retirement and its impact

In 2006 a major report from the National Bureau of Economic Research the effects of retirement on physical and mental health outcomes was published. This study demonstrated that complete retirement leads to 5-16 percent in difficulties associated with mobility and daily activities; a 5-6 percent increase in illness conditions and 6-9 percent decline in mental health, over a post-retirement period of six years. This study also reported that the adverse health effects are mitigated if the individual is married and has social support, continues to engage in physical activity post retirement, or continues to work part-time upon retirement. (Dhaval, Rashad & Spasojevic, 2006).

The following year a study identified those who are at risk for a decline of life satisfaction during the retirement transition (e.g., those with poor physical health, low Social Economic Status or who were not married) and who may, therefore, profit most from retirement planning interventions (Pinquart & Schinder, 2007).

|

The financial factors involved in pre-retirement planning were studied in 2008 and the analyses revealed substantial support for the role of psychological factors in the retirement planning process. This study supported the development of psychologically based models of planning, as well as applied implications for those who seek to understand the psycho-motivational forces that underlie tendencies to plan and save (Hershey, et al., 2007).

|

A 2008 study found a pattern with signs of poor adjustment negatively affected by a forced choice to retire early with very high levels of distress and low satisfaction which supports the notion of raising the age of retirement might lessen such distress (Isaksson,& Johansson, 2008).

In 2009 in addressing pre-retirement planning a caution was given that when attempting to create and deliver interventions designed to increase

- Financial stability;

- Physical health;

- Interpersonal and leisure activities;

- Post-retirement work planning;

that policy makers and counselors cannot apply a broad-brush, one-size-fits-all approach. Rather, proposed interventions should take into account and be designed around the specific variables known to influence planning within that particular domain.The exception to this was goal setting, which was the one consistent predictor of planning across all domains. Given that goals are malleable and not fixed characteristics of an individual, goal setting could represent an important ingredient in the design of interventions promoting holistic retirement planning (Petkoska & Earl, 2009).

|

In 2010 the Process of Retirement Planning Scale was developed and is know as the PRePSwhich assesses cognitions surrounding future community and familial roles, goals for future roles, decisions about preparation for role change, and the preparatory behaviors undertaken to fulfill previous psychosocial goals. PRePS allows researchers to test the theory that the transition to retirement can be eased by practicing anticipatory socialization with future roles (Noone et al., 2010). In 2013 the PRePS was researched in Turkey and it was concluded that the Turkish version of the PRePS had sufficiently high reliability and validity to justify its use as a tool to measure employees’ retirement planning behaviors in Turkey (Gunay, 2013).

|

|

Items Comprising the PRePS According to the Stage of the Process Model

Retirement representation

I’ve thought a lot about my future finances.

I often compare my current financial position with the financial position I would like to have in retirement.

I have a clear understanding of financial issues for retired people.

I often talk to my family about financial issues for retired people.

I think a lot about my long-term health.

I often compare my current health with how I would like it to be in the future.

I have a clear understanding of the importance of health for older people.

I often talk to my family about our future health.

I’ve thought a lot about how I will spend my time in retirement.

I often compare how I spend my time now with how I would like to spend my time in retirement.

I have a clear understanding of how retired people spend their time.

I often talk to my family about how retired people spend their time.

I’ve thought a lot about my roles as a retired person within my family.

I’ve thought a lot about my roles as a retired person within my community.

I have a clear understanding of how people’s roles can change when they retire

I often compare my current roles with the roles I would like to have as a retired person.

I often talk to my family about the roles of retired people.

I often speak to retired people about what it’s like to be retired.

Retirement Goals

I have specific goals regarding the financial position I want in retirement.

I have specific goals for my long-term health.

I have specific goals regarding how I want to spend my time in retirement.

I have specific goals regarding the future roles I would like to hold as a retiree.

The Decision to Prepare for Retirement

It’s too early for me to start thinking about my retirement finances.

I’d rather deal with any financial issues closer to retirement, rather than making financial provisions now.

I know that people in my age group are making financial preparations for retirement.

It’s worthwhile to make financial provisions for retirement.

It’s too early for me to consider my long-term health.

I’d rather deal with any health issues when they arise rather than prepare for them now.

It’s too early for me to start thinking about how I will spend my time in retirement.

I’d rather decide what to do with my time once I retire, rather than think about it now.

I know that people in my age group are developing new ways to spend their time.

It’s worthwhile to develop new activities for retirement.

It’s too early for me to consider my roles as a retired person.

I’d rather deal with any issues regarding my future roles when they arise, rather than prepare for them now.

I know that people in my age group are preparing for changes to their roles.

It’s worthwhile to prepare for changes to my roles as a retired person.

Preparing for Retirement

If I was forced to retire today, I would have enough money to cope well with retirement.

If I was forced to retire at age 65, I would have enough money to cope well with retirement.

Members of my household are able to put aside or invest a sufficient proportion of our income.

By the time I retire, I will have sufficient income to ensure the standard of living I want in retirement.

By the time I retire, I will own a house without a mortgage.

By the time I retire, I will have enough money to pay for any unexpected expenses.

I only eat foods that will benefit my long-term health.

I avoid all unhealthy behaviors.

I try to keep physically active (e.g., by taking regular walks, playing sports, or doing yoga, etc.).

I never get medical screening for diseases such as cancer, diabetes, and heart disease.

I never have general medical check-ups.

There are many things I could do with my time if I was forced to retire today.

I have recently taken up new interests, activities, or hobbies.

I have many interests outside of work that I would like to pursue.

I’m starting to separate myself from my work.

I am reducing or will soon reduce my work hours.

(Noone et al., 2010)

|

|

Retirement-Pre-retirement Mental Health and Physical Well-being Considerations

Assessment of the Retirement Process

In 2017, 28 measures assess the were identified which assess the process retirement. These measures assess retirement attitudes, planning, decision making, adjustment and satisfaction with retirement (Rafalski, et al., 2017). 20 of these measures assessed retirement attitudes, plans and decision making. 5 assessed adjustment to retirement and only 2 measured retirement satisfaction. The measures are used to assess how people (1) Attitudes about retirement (2) Retirement planning, (3) Retirement decision making, (4) Adjustment to retirement and (5) Satisfaction from such experience. Together these five stages represent the process of retirement identified by Wang in 2007 (Wang, 2007). In 2014 an example of this range of factors was presented with a focus on 7 variables:

- Age

- Annual Income

- Level of Education

- Marital status

- Problem-solving skills

- Attitudes toward future

- Long-term illness (Wang et al., 2014)

|

|

The Retirement Process Examined

1. Attitudes about Retirement: this is how individuals evaluate a given object or event and are a function of psychosocial, economic and cultural influences. For example those with a positive attitude toward retirement tend to be financially secure, socially integrated, older, married and male. In terms of the retirement process, workers’ positive attitudes towards retirement have been shown to predict higher level of retirement planning.

2. Retirement Planning: This second stage of the retirement process has been conceptualized as a multi-stage process beginning with representations or understandings of the future event, leading to goad development and uptake of behaviors that meet prior goals. Retirement planning is also understood to extend beyond financial preparations to include: health, lifestyle and psychosocial planning (e.g. preparing for new social roles). Research supports the belief that retirement planning predicts satisfaction and good health in retirement. Those who prepare for retirement tend to rate the transition as voluntary and even if retirees perceived they were forced into retirement, they report better satisfaction if they had been able to make at least some preparations. It is for this reason that retirement planning, along with health, lifestyle and other factors, influences the decision to retire.

3. Retirement Decision: This third stage is the push pull phase of retirement planning. On one hand negative factors such as poor health or job dissatisfaction push people out of work while the desire for more leisure time can pull people into retirement. A lack of choice in the retirement decision is associated with maladjustment to retirement, dissatisfaction with retirement, and poor health. The nature of the retirement decision has been shown to be one of the strongest predictors of such retirement outcomes as satisfaction and adjustment.

4. Adjusting to Retirement: Adjustment requires the ability to cope with change and is often marked with a phase in which retirees grow accustomed with the routine of being retired. Successful adaption is associated with mental and physical health, retirement planning and positive financial status.

5. Satisfaction with Retirement: This final stage of retirement satisfaction evaluation is a function of the four previous stages of the retirement process. It is dependent on various factors such as labor, family interactions, culture and economy. The individual’s interaction with these factors can determine the result of the retirement process. The evaluation of satisfaction can happen moments that will lead to positive or negative results. For example, an individual can present different results due to the ever-changing nature of human life and its surroundings. Unfortunately, it has been found that a positively perceived and well voluntary transition from full-time work does not always lead to good outcomes. For example: it is possible to adjust to retirement and receive no satisfaction from it, while positive changes such as having more time and leaving a stressful job do not guarantee successful adjustment. Other factors such as health, marital status, age and gender are often associated with satisfaction and the other stages of the retirement process.

(Rafalski, et al., 2017)

|

|

Downside of Retirement

Research has demonstrated that being fully retired or unemployed was associated with higher odds of having a high level of psychological distress than being in paid work for men and women aged less than 65 years. Being fully retired was also associated with higher odds of having a high level of psychological distress in men aged from 65 to 74 years, while there was no significant difference in the odds for women in the same age group. There was higher proportion of men retired due to being made redundant than women, and higher proportion of women retired to care for family or friends than men. Retirement due to being made redundant was associated with higher odds of having a high level of psychological distress in men aged from 55 to 79 years, and in women aged from 55 to 64 years. Retirement due to caring for family or friends was associated with higher odds of having a high level of psychological distress in women aged from 55 to 69 years and in men aged from 60 to 64 year (Vo, et al., 2015)

The defining features of later-life crisis are different to crisis that occurs earlier in adulthood in certain ways, while also being notably similar in other ways. Similarities include the presence of stressful endings, new beginnings, self-questioning, instability of life structure and emotional upheaval; these occur in crises in early adulthood and midlife too. There are also several key differences: firstly, crisis events earlier in adulthood are defined by the challenges of becoming embedded in adult roles that come to feel ensnaring and engulfing, while later life crisis is defined by the challenges and emotional difficulties of losing those roles, as well as feelings of marginalization and isolation; secondly, crises in early adulthood rarely involve illness and bereavements while many later-life include one or both of these events (Robinson & Stell, 2015).

In retirement, men need to be challenged to be healthy in mind and body. To do so requires that they not take it easy by devoting themselves to gardening, golfing and napping because a absence of challenges can have the same effect as too much stress, compromising their physical and mental health. It is recommended that for men’s optimal well-being they need to stay engaged with their own interests as well as with other people. Doing too little or too much can lead to similar symptoms, such as anxiety, depression, appetite loss, memory impairment, and insomnia. (Harvard Men’s Health Watch, 2015).

|

|

Tips for adjusting to retirement

1. Have places to be every week and make commitments. This helps to create structured time that many people need to feel “normal.”

2. Pursue hobbies that involve creativity, rather than repetitive tasks.

3. Volunteer, especially if it allows you to be of service. Some research suggests

it is healthy to help others.

4. Learn something new, especially if it involves interacting with other people,

like playing an instrument or studying a second or third language.

(Harvard Men’s Health Watch p. 5, April 2015)

|

|

A 2017 study found that retirement bring the threat of going from somebody to nobody overnight, of being a nonentity experiencing nothingness, generates an enormous amount of anxiety. Loss of status, loss of recognition, loss of income and emotional stress are found to be present in post-retirement reality where the connotation of letting go can seem overwhelmingly negative. Anxiety is a state of distress and/or physiological arousal in reaction to stimuli including novel situations and the potential for undesirable outcomes and that anxiety is common after retirement this study points out. Retirees who have attached their sense of identity and value to their work can become depressed if they are not able to reassign themselves properly to new interests. It can become chronic and may stimulate suicidal ideation and attempts. (Sekhri & Sekhri, 2017).

Research into the excessive drinking among the newly retired has demonstrated that loss of identity, coping with physical and psychological problems, an overarching societal and social culture surrounding alcohol and the interrelationship between social life, alcohol use and heavy drinking are important factors that need be addressed clinically and preventively, and specifically for individuals experiencing very late-onset alcohol use disorder For this reason mental health professionals need to work at preventive strategies with psychoeducational programming to help retirees ward off this negative outcome from retirement (Emiliussen et al, 2017)

The transition to retirement implies significant changes in daily routine and in the social

environment. More specifically, it requires more self-directed efforts in order to stay socially engaged. For this reason, for those who suffer from loneliness while still working, the transition to retirement could result in increased depressive symptoms due to the lack of structured daily routine. Although many seniors manage to easily transition into retirement, lonely older workers are at increased risk for maladjustment and the experience of depressive symptoms following retirement. This group could perhaps benefit from interventions aimed at increasing daily social interactions and establishing a socially satisfying routine (Segel-Karpas, Ayalon & Lachman, 2018).

A 2018 study investigated the role of social and mental occupational characteristics in cognitive decline after retirement. The findings were that workers retiring from occupations characterized by high levels of social stimulation may be at risk of accelerated cognitive decline with advancing age (Grotz et al., 2018). This study stresses it is necessary to understand how loss of exposure to the work environment due to retirement can be compensated by social stimulation so there is a need for future retirees to be helped to identify sources for such social stimulation and the prepare for their own retirement.

Self-esteem is impacted by the planning for retirement five years out from actual retirement and then the decrease halts during the year of retirement (Bleidorn & Schwaba, 2018). This finding emphasizes the need for good preventative mental health intervention to help pre-retirees to develop a productive post-retirement plan of action in which their self-esteem will not be negatively impacted.

|

Upside of Retirement

A 2016 study found that enjoyment of everyday activities increased after retirement and remained elevated for at least 12 months. The conclusion being that spending time at full-time work appears to constitute a relative deficit to enjoying everyday activities ( Olds, et al., 2016),

Research has shown that mental health and well-being of working senior adults post retirement is better in comparison to non-working retired seniors (Jain et al., 2017). This study found that seniors who continue working post retirement, stay engaged in their communities, and spend more time with family and friends, and have better mental health than others. This study recommended that seniors should continue to work part time or full time after retirement, in order to ease into the retirement status slowly. It was recommended that seniors should not only plan their retirement financially but should also make plans to incorporate other kinds of work or hobbies into their post-retirement (Jain et al., 2017).

Following retirement, time no longer spent in work flowed mainly to household chores,

sleep, screen time and quiet time (e.g. reading). Mental health improved overall. Changes in the activity composition were significantly related to conditional changes in depression, stress, and self-esteem, but not to anxiety, well-being or life satisfaction, Following retirement, replacing work with physical activity, and to a lesser extent sleep, is associated with better mental health (Olds et al., 2018).

|

Most Current Perspective on Retirement and Retirement Planning

In a recent major study, it was found that adaptation to retirement requires considering care comprehensively in the physical, mental, and social areas. Retirement from work implies a transition that is accompanied by losses, such as the loss of the role of worker, loss of status, and loss of social relations. The incidence of these losses on subsequent well-being will depend on personal factors, so it is essential to pay special attention to all these variables. This study also reviewed the losses that affect people’s quality of life and health in the face of adjustment to retirement. Physical, cognitive, motivational, financial, social, and emotional resources were examined (Hurtado & Topa, 2019). This study suggested that when designing seminars, courses, or workshops for retirement preparation, one should take into account the diversity of resources. However, their research also demonstrated that that preparation could be improved, and it would be interesting to orient interventions for potential retirees to maintain and increase the resources that are needed. On another hand, there is also a need to train professionals to help people who make the transition to retirement in terms of social resources and to minimize economic resource decreases. There is a need to encourage the development of motivational resources through volunteer service or other life facts associated with retirement. People’s loss of motivational resources in different vital moments could also affect the relationships between their adaptation to retirement (Hurtado & Topa, 2019).

|

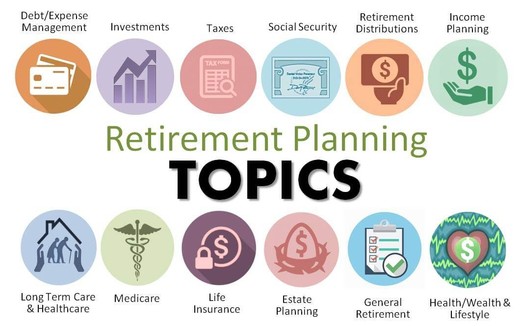

Financial Planning for Retirement

|

Watch this video before you address the Financial Planning for Retirement:

|

|

Top 10 Ways to Prepare Financially for Retirement

Financial security in retirement doesn’t just happen. It takes planning and commitment and, yes, money.

Facts

1. Fewer than half of Americans have calculated how much they need to save for retirement.

2. In 2016, almost 30 percent of private industry workers with access to a defined contribution plan (such as a 401(k) plan) did not participate.

3. The average American spends roughly 20 years in retirement.

4. Putting money away for retirement is a habit we can all live with.

Remember…Saving Matters!

1. Start saving, keep saving, and stick to your goals

If you are already saving, whether for retirement or another goal, keep going! You know that saving is a rewarding habit. If you’re not saving, it’s time to get started. Start small if you have to and try to increase the amount you save each month. The sooner you start saving, the more time your money has to grow (see the chart below). Make saving for retirement a priority. Devise a plan, stick to it, and set goals. Remember, it’s never too early or too late to start saving.

2.Know your retirement needs

Retirement is expensive. Experts estimate that you will need 70 to 90 percent of your pre-retirement income to maintain your standard of living when you stop working. Take charge of your financial future. The key to a secure retirement is to plan ahead. Start by requesting Savings Fitness: A Guide to Your Money and Your Financial Future and, for those near retirement, Taking the Mystery Out of Retirement Planning. (See below to order a copy.)

3.Contribute to your employer’s retirement savings plan

If your employer offers a retirement savings plan, such as a 401(k) plan, sign up and contribute all you can. Your taxes will be lower, your company may kick in more, and automatic deductions make it easy. Over time, compound interest and tax deferrals make a big difference in the amount you will accumulate. Find out about your plan. For example, how much would you need to contribute to get the full employer contribution and how long would you need to stay in the plan to get that money.

4. Learn about your employer’s pension plan

If your employer has a traditional pension plan, check to see if you are covered by the plan and understand how it works. Ask for an individual benefit statement to see what your benefit is worth. Before you change jobs, find out what will happen to your pension benefit. Learn what benefits you may have from a previous employer. Find out if you will be entitled to benefits from your spouse’s plan. For more information, request What You Should Know about Your Retirement Plan. (See back panel for more information.)

5. Consider basic investment principles

How you save can be as important as how much you save. Inflation and the type of investments you make play important roles in how much you’ll have saved at retirement. Know how your savings or pension plan is invested. Learn about your plan’s investment options and ask questions. Put your savings in different types of investments. By diversifying this way, you are more likely to reduce risk and improve return. Your investment mix may change over time depending on a number of factors such as your age, goals, and financial circumstances. Financial security and knowledge go hand in hand.

6. Don’t touch your retirement savings

If you withdraw your retirement savings now, you’ll lose principal and interest and you may lose tax benefits or have to pay withdrawal penalties. If you change jobs, leave your savings invested in your current retirement plan, or roll them over to an IRA or your new employer’s plan.

7. Ask your employer to start a plan

If your employer doesn’t offer a retirement plan, suggest that it start one. There are a number of retirement saving plan options available. Your employer may be able to set up a simplified plan that can help both you and your employer.

8. Put money into an Individual Retirement Account

You can put up to $5,500 a year into an Individual Retirement Account (IRA); you can contribute even more if you are 50 or older. You can also start with much less. IRAs also provide tax advantages. When you open an IRA, you have two options – a traditional IRA or a Roth IRA. The tax treatment of your contributions and withdrawals will depend on which option you select. Also, the after-tax value of your withdrawal will depend on inflation and the type of IRA you choose. IRAs can provide an easy way to save. You can set it up so that an amount is automatically deducted from your checking or savings account and deposited in the IRA.

9. Find out about your Social Security benefits

Social Security pays benefits that are on average equal to about 40 percent of what you earned before retirement. You may be able to estimate your benefit by using the retirement estimator on the Social Security Administration’s Website, www.socialsecurity.gov . For more information, visit their Website or call 1-800-772-1213.

10. Ask Questions

While these tips are meant to point you in the right direction, you’ll need more information. Read our publications listed on the back panel. Talk to your employer, your bank, your union, or a financial adviser. Ask questions and make sure you understand the answers. Get practical advice and act now.

For More Information:

Visit the Employee Benefits Security Administration’s Website at www.dol.gov/agencies/ebsa

to view the following publications:

1. Savings Fitness: A Guide to Your Money and Your Financial Future Click Here to download

2. Taking the Mystery Out of Retirement Planning Click Here to download

3. What You Should Know About Your Retirement Plan Click Here to download

4. Filing a Claim for Your Retirement Benefits Click Here to download

5. Women and Retirement Savings Click Here to download

6. Retirement Toolkit Click Here to download

7. A Look at 401k Plan Fees Click Here to Download

To order copies, contact EBSA electronically at www.askebsa.dol.gov or by calling toll free 1-866-444-3272.

The following Websites can also be helpful:

AARP: www.aarp.org

American Savings Education Council: www.choosetosave.org/asec

Certified Financial Planner Board of Standards: www.LetsMakeAPlan.org

Consumer Federation of America: www.consumerfed.org

The Actuarial Foundation: www.actuarialfoundation.org

U.S. Department of the Treasury: www.irs.gov/retirement

U.S. Securities and Exchange Commission: www.investor.gov

This Message is from: Employee Benefits Security Administration of the United States Department of Labor

|

|

|

5 Traits of Successful Retirement Planning

From: https://blog.admiral.kendal.org/5-traits-of-successful-retirement-planning?

1. Talk with Your Spouse and Family

The first thing you will need to do is discuss future goals and plans with your spouse and/or your family. Some spouses may be more willing to talk about retirement living than others. If your spouse is not on the same page as you, it’s important to have a discussion about it. Be willing to listen to their reasoning, emphasize the need to make a plan and be prepared with resources. Be sure to brainstorm together your goals for the future, determine how much money you will need to live well and research the best options that fit you both. Once you have a plan in place, be sure to share with the rest of your family. Let them know your goals and wishes so they can be on the same page with you.

2. Have a Planning Team in Place

Along with planning with your spouse and family, you should also seek professional “teammates.”

(1) Your Doctor- Let your doctor in on the plan. Your doctor knows your physical and mental health and can be an asset in helping you determine what living option is best. They can also offer nutritional and fitness advice.

(2) Financial Planner-Hiring a financial planner to analyze your finances can be very beneficial. They can study your finances to help you determine which living arrangements fit your budget. Financial planners can also help you find financing options for long-term care.

(3) Lawyer-If you don’t already have a lawyer, you should think about hiring one that is well-versed in drawing up documents to designate a power of attorney should you ever need one in the future. Your selected power of attorney can make medical decisions and pay bills on your behalf if you are unable to do so yourself. If you haven’t already, you may also want to draft a will or update an existing one with the help of your lawyer.

(4) Behavioral Health Consultant-A mental health professional who will assist you to insure that you have an emotionally, socially and physically sound plan for retirement.

3. Plan for Potential Long-Term Care Needs

Somewhere between 50 to 70 percent of older adults will require long-term care (such as assisted living or memory care) at some point in their lives. This is why it’s a good idea to financially plan for this stage in your life in case you should ever need long-term care. One way to financially prepare for long-term care needs is to get long-term care insurance (LTCi) policy. An LTCi policy can be expensive but can help pay for long-term care services.

4. Explore Housing Options

There are many housing options to choose from. The trick is to find the one that fits you. For example, there is independent living, assisted living, aging in place in your own home and more.One of the most popular choices is a continuing care retirement community (also known as a CCRC or Lifecare community). A Lifecare community offers independent living, assisted living, skilled nursing and rehab and memory care all on one campus. The benefit of having all levels of care in one place is you don’t have to move around if your needs ever change. Rather, you can stay in a community you are already acclimated to and remain close to friends.

5. Increase Your Chances for a Healthy Future

To ensure a healthy future, be sure to take great care of yourself. Creating or continuing healthy habits such as exercise and proper nutrition is a good place to start. Be sure to get regular checkups with your doctor. If you aren’t already physically active, consult with your doctor to find exercises that work best for you.

|

|

Role Potential for Behavioral Health Providers in Retirement Planning

|

1. Become a Retirement Transition Consultant

Mental Health providers ought to take a proactive approach to addressing the needs of older adults who are transitioning from their careers through consultation and these providers can market themselves to organizations as Retirement Transition Consultants who meet with employees to discuss the transition from work to the next phase of life. This role could then be used to assess for risk factors (e.g., poor sense of self, outside the job-career role, poor social support) (Westefeld et al., 2015). The issues these Retirement Transition Consultants could cover include: presence of psychiatric diagnoses, physical illness, personality variables, social support, career issues, financial resources, autonomy and mobility, and cognitive loss (Westefeld et al., 2015).

|

2. Utilize a Multicultural Interventionist Model

Those who work with older adults should attend to the influence of cultural expectations, biases, values, and the multitude of transitions that accompany aging. For instance, cultural messages about loss of freedom, dependence on others, or contribution to society may influence clients’ distress. Recent literature has also emphasized the necessity of sensitivity to intersecting cultural identities. One example of these intersecting identities to which providers should attend is gender, age, and the generational cohort of the individual. The cultural importance of work to men’s identities leads to increased suicide risk when employment is lost. These providers must be sensitive to the intersection between how individuals’ cultural identities contribute to their distress vis-a`-vis the various transitions that accompany aging and the cultural shame that might accompany feelings of helplessness or thoughts of suicide following these transitions (Westefeld et al., 2015).

|

3. Provide Psychoeducation in the Community

Providers have a responsibility to disseminate their knowledge about suicide risk in older adults. They need to provide psychoeducational workshops to the general public, because these might help laypeople to better understand the added risk of suicide for older adults. The challenge will be to locate and gain access to groups of older adults for dissemination of information. Providers might consider engaging community-based organizations such as park districts, churches, or local governments to identify potential audiences of older adults and involving agencies that serve older adults in outreach efforts. In this way, Transition Consultants can provide guidance to professionals who work closely with older adults (Westefeld et al., 2015). It is important that counseling and psychoeducational programs for retirement should consider how to tailor the message and support to different personality types and gender given there is real heterogeneity in retirement in that women’s personality traits play a greater role in satisfaction in retirement than do men’s (Kesavayuth et al.,2016).

|

4. Introduce the Importance of increasing physical activity pre and post retirement

Retirement is a major life transition which affects lifestyle. Research has demonstrated that older retirement age, higher occupational status and fewer chronic diseases were associated with greater increase in physical activity during transition to statutory retirement (Stenholm et al., 2016). For this reason, it is imperative that Transition Consultants include in their programming emphasis on increasing physical activity of participant pre and post retirement. In another study intervention approaches for older adults to increase their physical activity encompassed: training of health care professionals; counselling and advice giving; group sessions; individual training sessions; in-home exercise programs; in-home computer-delivered programs; in-home telephone support; in-home diet and exercise programs; and community-wide initiatives. These approaches had positive outcomes. Studies on older adults more generally indicated that a range of interventions might be effective for people around retirement age with the positive increase of physical activity (Baxter, et al., 2016).

|

|

Heart Matters’ 20 Tips for a Happy Retirement

1. Get your finances in order

Organize your money so you can work out what you’ll have to live on. Gradually reducing your spending in the lead up to retirement will make it easier to adjust. Track down any old pensions, claim your state pension and check what other benefits you can claim.

2. Wind down gently

Ensure a smoother transition by retiring in stages. By easing off your workload over several years, you’ll be able to get used to the idea of not working and fill your time in other ways. Ask your employer if you can cut back your working hours.

3. Prepare for ups and downs

There may be times when you feel lonely or a bit lost, which is normal. If ill health or changes in your relationships temporarily scupper your plans, accept that this has happened and get your back-up plan in action. Think positively and share any concerns with others.

4. Eat well

Make sure you eat regular meals, especially if your previous pattern, while at work, was to snack. Take advantage of the extra time on your hands and explore healthy cooking options.

5. Develop a routine

You may find it feels more normal to continue getting up, eating and going to bed at roughly the same time every day. Plan in regular activities such as voluntary work, exercise and hobbies. This will keep things interesting and give you a purpose.

6. Exercise your mind

Government studies have shown that learning in later years can help people stay independent, so use your free time to continue to challenge yourself mentally, whether it’s learning an instrument or a language or getting a qualification.

7. Keep physically active

We should all aim to do at least 150 minutes of moderate-intensity physical activity a week, so build up to this if you haven’t made exercise a normal part of your life previously. Fresh air and exercise is an instant mood booster and instrumental in maintaining your wellbeing.

8. Make a list

Writing down your aims may help you focus on what you really want to achieve – like a ‘to do’ list. Work out what you can afford to do and schedule time to make it happen, so you experience a sense of accomplishment, as you would have done at work.

9. Seek social support

For many people, work can form a big part of their social life and it’s common to feel at a bit of a loose end once you retire. Fill the gaps by joining clubs and groups.

Find out about the social and physical benefits of walking groups.

10. Make peace and move on

Don’t spend your retirement dwelling on your working days. Accept that you’ve done all you can in that job and focus on your next challenge. You’ve still got lots to achieve.

11. Go for a health check

Prevention is better than cure, and now is the perfect time to get Health Check to help prevent heart disease, stroke, diabetes, kidney disease and certain types of dementia.

Everyone between the ages of 40 and 74, who has not already been diagnosed with one of these conditions or have certain risk factors, will be invited once every five years to have a check to assess their risk of these age-related illnesses and will be given support and advice to help them reduce or manage that risk.If you’re in this category but haven’t had a check in the last five years, you can ask your doctor for one.

12. Keep in touch with your friends from work

Just because you are retiring doesn’t mean you have to lose touch with the group of friends you made in your workplace. Why not make arrangements for regular catchups? Or, you might want to use some of your new leisure time to catch up with old friends that you haven’t seen for a while. If you enjoy party planning, find an excuse to get everyone together and have fun arranging the perfect garden or dinner party, anniversary celebration or other special occasion.

13. Pamper yourself

After decades of hard work, you are due some ‘me time’. Whether your idea of indulgence is a city break, a day trip to a spa or a small pleasure like dining out or going to the cinema, schedule some time for a well-deserved treat.

14. Practice mindfulness

Practicing mindfulness has become more popular than ever in the last decade as a strategy to relieve stress, anxiety and depression. Research, such as a 2009 study from Goethe University in Germany, has shown that meditation strengthens the hippocampus, the area of the brain that is important for memory, and slows the decline of brain areas responsible for sustaining attention. There are no set guidelines for how often you should meditate for optimal result, but a handful of experiments suggest that a mere 10 to 20 minutes of mindfulness a day can be beneficial—if people stick with it.

15. Give back to the community

Ever thought of volunteering? Perhaps you’d enjoy getting involved with your local youth club, animal rescue center, environmental organization or elderly support group.

There are plenty of charities that would welcome a helping hand, Organizations like Goodwill and Salvation Army offer the opportunity to help out in their shops, in a furniture or electrical store, with fundraising and at lots of different types of events. Why not sign up for a charity event to give you a goal to work towards?

16. Be one with nature

Fresh air and exercise is an instant mood booster and instrumental in maintaining your wellbeing. Why not incorporate a walk in the woods or a nearby park into your daily routine? This is an ideal way of achieving the recommended minimum of 150 minutes of physical activity per week.

17. Travel more

Always dreamt of going on an around-the-world cruise, a wine-tasting trip through Italy, or a simple camping expedition in the Welsh valleys? Now you can finally make those long-held plans a reality, depending on your health and budget limitations.

If longer trips aren’t practical, mini breaks may be a good alternative – or even days out to places you’ve never visited before.

18. Get a new pet

Could you house a rescue cat or dog in need of a new home? Research has shown that our furry friends have a positive effect on our health and wellbeing.

According to pet researcher Allen R. McConnell, a professor of psychology at Miami University, people with pets are generally happier, more trusting, and less lonely than those who don't have pets. They also visit the doctor less often for minor problems.

One reason for that may be that your pet gives you a sense of belonging and meaning, Prof McConnell says. "You feel like you have greater control of your life."

19. Push your boundaries

It’s easy to get stuck in a rut, both health-wise and in general, and doing something different can be a refreshing change. Some people have found that simple changes, such as trying a tasty new recipe, finding a different hairdresser or joining an exercise class they haven’t done before gives them a new zest for life.Use your free time to continue to challenge yourself mentally, whether it’s learning an instrument or a language or getting a qualification

20. Take up a new project

Finally, you have time to get stuck into all those things you’ve been meaning to do but never got round to. Mapping your family tree, building a shed, planting a veg patch… the list goes on, but now you can actually do what you’ve always wanted to.

- Need inspiration? Have a look at our features on gardening, healthy baking, and cycling groups.

- Read our feature about retirement.

- Read how volunteering can help you beat loneliness.

Available at: https://www.bhf.org.uk/informationsupport/heart-matters-magazine/wellbeing/retirement/retirement-tips

|

|

8. Make exercise fun and, if walking is your exercise, walk fast9. Think income not investments10. Leave behind more wealth than you had when you first retired11. Create and maintain a comprehensive investment strategy12. Don’t overlook taxes13. Keep a schedule and structure follow 7 other overlook retirement skills14. Research the best places to retire and go there15. Make your travel dreams a reality16. Think positively about aging17. Some researcher thing aging is …optional?18. Avoid retirement depression (it is more common than you think)19. Spend time with the grandkids20. Have you found your “Ikigai” (Okinawan term for Reason for Living”)21. Make sure your retirement planning includes your spouse and love ones22. Single? Here are tips for you23. If you have a health setback, adopt a positive outlook24. Find a motto for your retirement plan - Put it on your refrigerator25. Protect yourself from fraud26. Stay married – especially if you are a man27. Devote time to retirement planning – even after you retire28. Think beyond funds and bonds29. Spend your savings (Safely)!30. Adjust to turning your perspective upside down31. Be social32. Be social with people outside your age group33. Choose the right time to start social security34. Come out of retirement for a career switch35. Hire a financial advisor36. Are you a family caregiver? Be careful to keep your own retirement on track37. Get a dog38. Don’t stop budgeting39. Keep learning about finances40. Be sure to plan your next big financial goal: Your Estate!41. Know your money personality42. Be realistic about what retirement will mean to your lifestyle43. Continually optimize your health insurance44. Don’t forget to plan for a long-term care need45. Prepare for awful things that are likely to happen46. Throw a retirement party47. Will a retirement survival pack help you to have a happier retirement?48. Watch a movie49. Optimize your resources to maximize your income and protection from risks50. Reverse your retirement51. Get out and do something amazing-it is not too late52. Cut housing costs53. Learn a new skill54. Get a coach: A Retirement Coach55. Follow the lessons of healthy 90 Year Olds56. Think about college in a whole new way57. Start a retirement planning club58. Forget retirement-Take a long vacation instead59. Keep making 5-year plans60. Not yet retired? Do some catch up savings61. Getting older? Be sure to take your RMD (require minimum distribution from your IRA)62. Think of yourself as young63. Stay inquisitive about the world around you64. Plan for a longer and healthier life in retirement65. Think about the big picture

Visit NewRetirement at: https://www.newretirement.com/

|

Retirement Coaching Websites:

InFRE - 4 Steps to Become a Certified Retirement Counselor (CRC)

Retirement-Online.com - Wendy The Retirement Counselor

|

References

Baxter, S., Johnson, M., Payne, N., Buckley-Woods, H., Blank, L., Hock, E., Daley, A.,

Taylor, A., Pavey, T., Mountain, G. & Goyder, E. (2016). Promoting and maintaining physical activity in transition to retirement: A systematic review of interventions for adults around retirement age. International Journal of Behavioral Nutrition and Physical Activity, 13:12. DOI 10.1186/s12966-016-0336-3

Bleidorn, W. & Schwaba, T. (2018). Retirement is associated with change in self-

esteem. Psychology and Aging, 33(4), 586-594. http://dx.doi.org/10.1037/pag0000253

Dhaval, D., Rashad, I. & Spasojevic, J. (2006). The effects of retirement on physical

and mental health outcomes. NBER Working Paper No. 12123. National Bureau of Economic Research: Cambridge, MA.

Emiliussen, J., Andersen, K. & Nielsen, A.S. (2017). Why do some older adults start

drinking excessively late in life? Results for an interpretiative phenomenological Study. Scandinavian Journal of Caring Services 31, 974-983. doi: 10.1111/scs.12421

Grotz, C., Mellon, C., Amieva, H., Andel, R., Dartigues, J.F., Adam, S. & Letenneur

(2018). Occupational social and mental stimulation and cognitive decline with

advance age. Age and Ageing, 47, 101-106. doi: 10.1093/ageing/afx101

Gunay, G. (2013). Turkish reliability and validity study of the Process of Retirement

Planning Scale: The example of Karabuk University. Turkish Journal of Geriatrics, 16(1), 84-96.

Haanen, J. (2019). Saving Retirement. Christianity Today.com. Retrieved at:

https://www.christianitytoday.com/ct/2019/march/cover-story-saving-retirement.html

Harvard Men’s Health Watch (2015). Retirement stress: Taking it too easy can be bad

for you, too. Harvard Men’s Health Watch, 2015, 5.

Hershey, D.A., Jacobs-Lawso, J.M., McArdle, J.J. & Hamagami, F. (2007).

Psychological foundations of financial planning for retirement. Journal of Adult Development, 14, 26-36. DOI 10.1007/s10804-007-9028-1

Hurtado, M.D. & Topa, G. (2019). Quality of life and health: Influence of preparation for

retirement behaviors though serial mediation of losses and gains. International Journal of Environmental Research and Public Health, 16. 1539. doi:10.3390/ijerph16091539

Isaksson, K. & Johansson, G. (2008). Early retirement: Positive or negative for well

being? Revista de Psicología del Trabajo y de las Organizaciones, 24(3), 284-301

Jain, S., Kuma, S. & Jain, S. (2017). Late-life engagement after retirement: Implications

for psychological well-being and distress in elderly. Indian Journal of Health and Wellbeing, 8(6), 525-529.

Kesavayuth, D., Rosenman, R.E. & Zikos, V. (2016). Retirement, personality and well-

being. Economic Inquiry 54(2), 733-750. doi:10.1111/ecin.12307

Noone, J.H., Stephens, C. & Alpas, F. (2010). The process of retirement planning scale

(PRePS): Development and validation. Psychological Assessment, 22(3), 520-531. DOI: 10.1037/a0019512

Olds, T., Burton, N.W., Sprod, J., Maher, C., Ferrar, K., Brown, W.J., van Uffelen, J. &

Dumuld, D.. (2018) One day you'll wake up and won't have to go to work: The impact of changes in time use on mental health following retirement. PLoS ONE 13(6): e0199605. https:// doi.org/10.1371/journal.pone.0199605

Olds, T.S., Sprod, J., Firrar, K., Burton, N., Brown, W. van Uffelen, J. & Maher, C.

(2016). Everybody’s working for the weekend: Changes in enjoyment of everyday activities across the retirement threshold. Age and Aging, 45, 850-855. doi: 10.1093/ageing/afw099

Petkoska, J. & Earl, J.K. (2009). Understanding the influence of demographic and

psychological variables on retirement planning. Psychology of Aging, 24(1), 245-251. DOI: 10.1037/a0014096

Pinquart, M. & Schinder, I. (2007). Changes in life satisfaction in the transition to

retirement: A latent-class approach. Psychology of Aging, 22(3), 442-455. DOI: 10.1037/0882-7974.22.3.442

Rafalski, J.C., Noone, J.H., O’Laughlin, K. & de Andrade, A.L. (2017). Assessing the

process of retirement: A cross-cultural review of available measures. Journal of Cross Cultural Gerontology, 32, 255-279. DOI 10.1007/s10823-017-9316-6

Robinson, O.C. & Stell, A.J. (2015). Later-life crisis: Towards a holistic model. Journal of

Adult Development, 22, 38-49. DOI 10.1007/s10804-014-9199-5

Segel-Karpas, D., Ayalon, L. & Lachman, M.E. (2018). Loneliness and depressive

symptoms: The moderating role of the transition into retirement. Aging and Mental Health, 22(1), 135-140.http://dx.doi.org/10.1080/13607863.2016.1226770

Sekhri, R. & Sekhri, A. (2017). Psychological consequences of anxiety or loneliness and

suicide ideation among retirees: A psycho-social review. Indian Journal of Health and Wellbeing, 8(1), 38-40.

Stenholm, S., Pulakka, A., Kawachi, I., Oksanen, T. Halonen, J.I., Aalto, V., Kivimaki, M.

& Vahtera, J. (2016). Changes in physical activity during transition to retirement: A cohort study. International Journal of Behavioral Nutrition and Physical Activity 13, 51. DOI 10.1186/s12966-016-0375-9

Vo, K, Forder, P.M., Tavener, M., Rodgers, B., Banks, E., Bauman, A. & Byles, J.E.

(2015). Retirement, age, gender and mental health: Findings from the 45 and up study. Aging & Mental Health, 19(7), 647-657. http://dx.doi.org/10.1080/13607863.2014.962002

Wang, W.C., Worsley, A., Cunningham, E. & Hunter, W. (2014). The heterogeneity of

middle-aged Australians’ retirement plans. Social Work Research, 38(1), 36-46. doi: 10.1093/swr/svu005

Wang, M. (2007). Profiling retirees in the retirement transition and adjustment process:

Examining the longitudinal change patterns of retirees' psychological well-being. Journal of Applied Psychology, 92(2), 455–474. doi:10.1037/0021-9010.92.2.455.

Westefeld, J.S., Casper, D., Galligan, P., Gibbons, S., Lustgarten, S., Rice, A., Rowe-

Johnson, M. & Yeates, K. (2015). Suicide and older adults: Risk factors and recommendation. Journal of Loss and Trauma, 20, 491-508. DOI: 10.1080/15325024.2014.949154

|

|

|